Even as the economic recovery plods ahead, many American consumers are refusing to come along. They're not spending freely -- and they have no plans to.

Many of them have steady income. They aren't saddled by high debts. They don't fear losing their jobs. Yet despite recent gains, they've lost so much household wealth that they're far more cautious about spending than before the recession.

Their behavior suggests that the Great Recession may have bred a new frugality that will endure well into the recovery. And because consumers fuel about 70 percent of the economy, their tightfisted habits means the rebound could stay unusually sluggish.

They had in mind people like Marjorie Feldman of suburban St. Louis, who retired three years ago as a systems analyst for a utility company. The stock investments in her retirement account have sunk 15 percent from 2007. The value of her home is down 20 percent.

"I had retired assuming I'd make money" off the investments, said Feldman, who's in her early 60's. "I just don't feel as confident in the economy, and I never will again. I won't spend money the way I used to."

Feldman's husband works full time in academia. She has a part time job preparing tax returns at H&R Block. But her prime earning years are behind her. "I don't think it will ever get back to where it was before," she said of her nest egg. "I won't spend money the way I used to."

To be sure, many shoppers, especially the wealthy, are buying into the recovery. Partly on the strength of consumer spending, the economy emerged from recession last year and has been growing steadily, if moderately, since. Major retailers logged solid sales in March. Employers have begun to add jobs, including a net increase of 162,000 in March. The stock market has risen 70 percent from its low in March 2009.

Yet many who became penny-pinchers during the recession are in no mood to start shopping again with abandon for clothes, cars and home additions. They've discovered the peace of mind that comes with rebuilding savings, shopping more prudently and learning to live with less..

Interviews with ordinary Americans suggest a new frugality endures even though consumer spending has risen for five straight months and retail sales for three. In the AP's new quarterly survey, a majority of economists agreed that a new frugality will persist even as the recovery gains firmer footing.

"Consumers will not run up multiple credit cards to their limits, and when buying a house the objective will not be to get the maximum square footage for which they can afford the payment. A higher savings rate will be in place for several years."

Jeff Thredgold, an economist at Thredgold Economic Associates, predicts "less impress-my-neighbor-type spending" in coming years. He isn't worried about losing his job in business development at an information technology company. What's led him to cut back spending is the sunken value of his condominium. He bought it in 2005 for about $270,000.

"I doubt right now it's cracking $100,000," Flowers said.

Household net worth -- the value of assets like homes, checking accounts and investments minus debts like mortgages and credit cards -- has risen for three straight quarters. But economists say consumers would need a stronger and prolonged increase in wealth to lead them to ratchet up spending. Net worth would have to rise an additional 21 percent just to get back to its pre-recession peak of $65.9 trillion.

Some economists put their hopes for the economy in the rich, who are spending more freely than the rest of the population. They hold out hope that this will encourage more hiring and stimulate spending by the less wealthy. More spending could increase companies' revenue, which allow them to boost hiring and pay. And that would lead their employees to spend more.

Royal Caribbean Cruises Ltd. returned to a first-quarter profit as more travelers vacationed on its ships and spent more money on board. And makers of luxury goods are benefiting from a release of pent-up demand for jewelry, watches and high-end furnishings.

High-end retailers have reported blowout results. Nordstrom's revenue in stores open at least one year jumped 16.8 percent last month. Saks' surged 12.7 percent.

McClaren Automotive has announced it will debut a $200,000 sports car in the U.S. next year. And business is picking up faster at high-end hotels than at mid-priced and budget hotels.

Whether spending by the wealthy will cause the less-well-off to spend freely, too, remains unclear. For now, though, many people have embraced a more frugal approach to spending.

Or maybe they've just learned to go without.

Jan Iris Smith, 57, and her husband of Cabin John, Md., put off furniture and clothing purchases after the stock market's collapse in early 2009. "We were counting on our income from our investments," said Smith, a psychotherapist whose husband is retired. "We just stopped pretending everything was going to be OK anytime soon."

Showing posts with label money stories. Show all posts

Showing posts with label money stories. Show all posts

Thursday

American Greed

Anyone ever watch this show on CNBC? It's on every Sunday and Wednesday night. I tuned in last night and found this one story outright ridiculous.

It follows 2 sisters that operate a business supplying bolts, nuts, and screws on machineries operated by our troops during the war in Afghanistan.

It's very important that these supplies get to the troops in a quick and fast manner. So the government usually pays a high shipping cost to have these delivered pronto!

These two hardworking sisters were able to accidentally stumble across a loophole with the way they can bill their buyers (US Government of Defense) extravagantly.

It started out innocently when they were shipping some supplies over to the buyer and mistakenly keyed in the wrong shipping cost. They realized that regardless of the shipping cost number billed, the automated system used to generate a check to reimburse them for the shipping would pay the amount billed.

For example, the government of defense orders $4 worth of supplies from them. They were able to bill the buyer $100,000 shipping charge on this transaction. Overtime, they realized they can enter in any amount for shipping and still get reimbursed by the automated bill payout machine.

They spent lavishly over this system glitch for years. They bought vacation homes, jetskis, traveled to New York for an expensive jewlery trip, gambled in Las Vegas, and opened a cookie business. They portrayed a very successful image.

Eventually, all "too good to be true" things must come to an end.

Greed was ultimately their downfall when the sisters inadvertently submitted an order twice in error. The order was for a $0.38 screw and they charged a whopping $998,000 as the shipping cost.

Up until now they were able to escape human detection until this machine declined their request due to a duplicate entry. This was when authorities were called in and they found the sisters had scammed them close to $21mm worth.

It wasn't long until the FBI knocked on their door. This was too much for one of the sister. She eventually took her own life while the other one was sent to jail.

Retirement Mistakes

Investing in your future especially in a retirment account takes time and discipline. You most likely won't see the money grow too fast anytime soon. Remember that slow and steady wins the race.

I've been contributing to my 401K since the age of 22. However, I made a costly mistake to cash it all out to use as a downpayment towards our first home. Since then, I've gotten back on track and is now contributing 15% of my paycheck towards my golden years.

Here are some other costly mistakes that people often make to detriment their retirement accounts. Are you one of these people?

1) Blowing retirement savings early

This happens when people switch jobs and are forced to decide on whether to roll their 401K into an IRA or cash it all out. And guess what the majority ends up doing?

2) Turning down free money

That's right, you heard me. The money is FREE and is waiting for you to collect it. But what do you do, you end up turning this free cash away. You do this by not participating in your company's 401K match.

I've seen this all too many times happening to friends and even current coworkers at my workplace. I ask them why not get a few hundreds to thousands of dollars for free each year. They reply with being lazy = lame.

3)Saving without a goal

Unfortunately, many of us get this magical retirement number wrong. We end up miscalculating the wrong retirment age and not meeting its goal by socking away the correct amount every month. Then when it comes time to retire, you just don't have enough to last you through.

4)Ignoring your investments

Your retirement assets require regular upkeep just like your house and your car. Ignore them and they could fall apart. Be sure to review and rebalance your investments at least once a year to make sure you're comfortable with the level of risk in your portfolio.

5)Procrastinating

Getting a late start is just as bad. For proof, look at the following examples.

Let's say a 25 year-old begins saving $3,000 a year, but stops after only 10 years. Over the next 40 years, she could expect that $30,000 investment to grow to more than $472,000, assuming an 8% return.

If the same investor waited until age 35 to begin saving and stashed $3,000 a year for 30 years, she could only expect to have about $367,000, assuming the same 8% annual return.

By waiting 10 years to start saving, you lose out on the benefits of time and compounding returns, not to mention over $100,000!

Monday

How much money is enough?

If you happened to see the recent lists of 2009 compensation packages for CEOs or hedge fund managers, you may have found yourself trying to wrap your head around some staggering numbers.

Larry Ellison made an estimated $84.5 million last year while hedge fund alpha-dog David Tepper took in about $4 billion.

What do those numbers mean? Was Tepper 473 times more "successful" than Ellison in 2009? And how do they compare to you? Let's say you're a Bay Area resident with a median individual income of around $50,000.

Ellison's compensation was about 1690 times yours. Does that sound about right for the respective jobs you did last year?

Leaving aside the arguments about whether or not such ratios are logically or morally out of whack, let's consider the meaning of this money from another perspective: what does a $4 billion or an $84 million, or $50,000 income mean in terms of personal satisfaction?

In other words, if you were making $4 billion a year, would you be happier? If so, how much happier? What if you (you, median Bay Area person, with a $50,000 a year income) were making $100,000 a year? Would that be enough? What about $200,000? $2 million?

Is there a point of diminishing returns -- an income level after which happiness stops increasing along with income?

***

Marty Nemko, a Bay Area career coach and radio host says his clients put "too much" emphasis on money when considering their career choices.

"I just saw a client who makes $500,000 a year, and he's pissed off that his peers are making $700,000. Like it's going to affect his quality of life!

There are legitimate cases in which more money does make a real difference in well being, Nemko says if you can't afford health care, for example but too often, he says, he sees people pursuing careers they would "never in a million years have chosen" simply because those jobs feed a consumptive, "designer-label lifestyle."

Be conscious of what you're trading away in the quest for a higher salary, Nemko cautions. "Normally, the people who make big dollars are the people who are bringing in big dollars for some other entity," he says. "They're corporate lawyers, bond traders, or they sell insurance -- stuff that may or may not make the world much better, and that they don't even like that much."

If you're still convinced that an increased income will improve your well being, Nemko has another important caveat: "What counts is after-tax dollars. If you fight for an extra $20,000 a year but you're really only getting $12,000 after taxes, how much is that really going to change your lifestyle?" he says.

So is there a magic number that Nemko pegs as sufficient for getting by happily in the Bay Area? In a recent blog post he details a plan for living well on $20,000 a year, but Nemko says the income-satisfaction point will vary depending on one's choices of things like housing, cars, and whether or not one spouse stays at home.

"I can't give one number" for how much is enough, he says.

***

Jean Chatzky, the financial editor for NBC's "Today Show," did come up with such a number after conducting a survey of 1,500 Americans in 2003 for her book "The Ten Commandments of Financial Happiness."

Chatzky says the amount of money required to "live comfortably" varies by region, but her survey of Americans' attitudes suggested that "once you've got enough to put food on the table, gas in the car, go out to movies occasionally and go on the occasional vacation, more money doesn't make you happier."

She found the point of diminishing happiness returns was about $60,000 per household, annually. In other words, after $60,000, gains in income didn't bring corresponding increases in happiness.

Like Nemko, Chatzky emphasizes that making more money to meet basic needs can significantly affect well-being. "When you look at what has the ability to make people miserable, the leading factor is health. If your health is not good and you are so poor that you are struggling on a day-to-day basis ... that's an economic problem."

Beyond these basic needs, Chatzky says what makes people happier is "having greater control over whatever money they have." Her survey reflected higher happiness ratings from people who "set goals for themselves and benchmarked those goals; people who paid their bills as they came in instead of saving up their bills to pay all at once; and people who saved something."

***

Nemko's and Chatzky's conclusions may come as a relief: forget keeping up with the Joneses (or the Ellisons and Teppers). The sacrifices aren't worth it.

As Chatzky puts it, "Measuring up doesn't help anybody. If you can get yourself to a place where you are really focused inward instead of outward, you're going to be significantly happier."

That may have been the end of the story, had I not called Justin Wolfers, associate professor of business and public policy at the University of Pennsylvania's Wharton School of Business.

In 2008, Wolfers and his Wharton colleague Betsey Stevenson published a study rebutting the so-called Easterlin paradox (the finding, in a 1974 paper by economist Richard Easterlin, that, while rich people within a country are happier than poor people, increases in a country's GDP do not correlate to an increase in national happiness).

(You can find a link to Wolfers' and Stevenson's paper, along with a good explanation of its context and reactions to it -- here.)

"I'm biased, of course," Wolfers told me, "but my sense is that most economists have gone from believing in that Easterlin hypothesis to believing it looks like income and happiness are quite strongly related."

OK, so maybe more money creates more happiness, but only up to a point, right?

Well, maybe not.

Wolfers says he and Stevenson are halfway through a new research paper investigating precisely that hypothesis, and so far, they've found it to be false.

"If you look for evidence that there's some level above which money is unrelated to happiness," Wolfers says. "You simply can't find it. Using American data, [from sources such as Gallup polls], it's true that people earning $50,000 are happier than those earning $25,000, people earning $100,000 are happier than those earning $50,000, and people earning $200,000 are happier than those earning $100,000."

So can we conclude then, that Larry Ellison is 169 times happier than you?

Well, not exactly. But Wolfers and Stevenson have, in fact, quantified the relationship between income and subjective reports of well-being.

"It's what we call a linear log relationship," Wolfers says. Translation: "At any point in the income scale, a 10 percent rise in income buys the same rise in happiness."

And the Wharton professors have found this formula holds cross-nationally, too. "A 10 percent rise in income for someone in Burundi buys about the same change in happiness as a 10 percent rise for people in the U.S.," says Wolfers. "That's the sense in which we say there's no evidence of satiation. There's no evidence of it running out at income level whatsoever."

(Wolfers' analysis spans multiple studies, but he says one of the recent Gallup polls he analyzed listed ">$500,000" as the highest income category.)

The upshot is that hedge fund honcho David Tepper would, in theory, need to earn an extra $400 million to see a 10 percent increase happiness. You, Bay Area median income earner, just need to find $5,000 more per year to make the same jump in your sense of well-being.

Larry Ellison made an estimated $84.5 million last year while hedge fund alpha-dog David Tepper took in about $4 billion.

What do those numbers mean? Was Tepper 473 times more "successful" than Ellison in 2009? And how do they compare to you? Let's say you're a Bay Area resident with a median individual income of around $50,000.

Ellison's compensation was about 1690 times yours. Does that sound about right for the respective jobs you did last year?

Leaving aside the arguments about whether or not such ratios are logically or morally out of whack, let's consider the meaning of this money from another perspective: what does a $4 billion or an $84 million, or $50,000 income mean in terms of personal satisfaction?

In other words, if you were making $4 billion a year, would you be happier? If so, how much happier? What if you (you, median Bay Area person, with a $50,000 a year income) were making $100,000 a year? Would that be enough? What about $200,000? $2 million?

Is there a point of diminishing returns -- an income level after which happiness stops increasing along with income?

***

Marty Nemko, a Bay Area career coach and radio host says his clients put "too much" emphasis on money when considering their career choices.

"I just saw a client who makes $500,000 a year, and he's pissed off that his peers are making $700,000. Like it's going to affect his quality of life!

There are legitimate cases in which more money does make a real difference in well being, Nemko says if you can't afford health care, for example but too often, he says, he sees people pursuing careers they would "never in a million years have chosen" simply because those jobs feed a consumptive, "designer-label lifestyle."

Be conscious of what you're trading away in the quest for a higher salary, Nemko cautions. "Normally, the people who make big dollars are the people who are bringing in big dollars for some other entity," he says. "They're corporate lawyers, bond traders, or they sell insurance -- stuff that may or may not make the world much better, and that they don't even like that much."

If you're still convinced that an increased income will improve your well being, Nemko has another important caveat: "What counts is after-tax dollars. If you fight for an extra $20,000 a year but you're really only getting $12,000 after taxes, how much is that really going to change your lifestyle?" he says.

So is there a magic number that Nemko pegs as sufficient for getting by happily in the Bay Area? In a recent blog post he details a plan for living well on $20,000 a year, but Nemko says the income-satisfaction point will vary depending on one's choices of things like housing, cars, and whether or not one spouse stays at home.

"I can't give one number" for how much is enough, he says.

***

Jean Chatzky, the financial editor for NBC's "Today Show," did come up with such a number after conducting a survey of 1,500 Americans in 2003 for her book "The Ten Commandments of Financial Happiness."

Chatzky says the amount of money required to "live comfortably" varies by region, but her survey of Americans' attitudes suggested that "once you've got enough to put food on the table, gas in the car, go out to movies occasionally and go on the occasional vacation, more money doesn't make you happier."

She found the point of diminishing happiness returns was about $60,000 per household, annually. In other words, after $60,000, gains in income didn't bring corresponding increases in happiness.

Like Nemko, Chatzky emphasizes that making more money to meet basic needs can significantly affect well-being. "When you look at what has the ability to make people miserable, the leading factor is health. If your health is not good and you are so poor that you are struggling on a day-to-day basis ... that's an economic problem."

Beyond these basic needs, Chatzky says what makes people happier is "having greater control over whatever money they have." Her survey reflected higher happiness ratings from people who "set goals for themselves and benchmarked those goals; people who paid their bills as they came in instead of saving up their bills to pay all at once; and people who saved something."

***

Nemko's and Chatzky's conclusions may come as a relief: forget keeping up with the Joneses (or the Ellisons and Teppers). The sacrifices aren't worth it.

As Chatzky puts it, "Measuring up doesn't help anybody. If you can get yourself to a place where you are really focused inward instead of outward, you're going to be significantly happier."

That may have been the end of the story, had I not called Justin Wolfers, associate professor of business and public policy at the University of Pennsylvania's Wharton School of Business.

In 2008, Wolfers and his Wharton colleague Betsey Stevenson published a study rebutting the so-called Easterlin paradox (the finding, in a 1974 paper by economist Richard Easterlin, that, while rich people within a country are happier than poor people, increases in a country's GDP do not correlate to an increase in national happiness).

(You can find a link to Wolfers' and Stevenson's paper, along with a good explanation of its context and reactions to it -- here.)

"I'm biased, of course," Wolfers told me, "but my sense is that most economists have gone from believing in that Easterlin hypothesis to believing it looks like income and happiness are quite strongly related."

OK, so maybe more money creates more happiness, but only up to a point, right?

Well, maybe not.

Wolfers says he and Stevenson are halfway through a new research paper investigating precisely that hypothesis, and so far, they've found it to be false.

"If you look for evidence that there's some level above which money is unrelated to happiness," Wolfers says. "You simply can't find it. Using American data, [from sources such as Gallup polls], it's true that people earning $50,000 are happier than those earning $25,000, people earning $100,000 are happier than those earning $50,000, and people earning $200,000 are happier than those earning $100,000."

So can we conclude then, that Larry Ellison is 169 times happier than you?

Well, not exactly. But Wolfers and Stevenson have, in fact, quantified the relationship between income and subjective reports of well-being.

"It's what we call a linear log relationship," Wolfers says. Translation: "At any point in the income scale, a 10 percent rise in income buys the same rise in happiness."

And the Wharton professors have found this formula holds cross-nationally, too. "A 10 percent rise in income for someone in Burundi buys about the same change in happiness as a 10 percent rise for people in the U.S.," says Wolfers. "That's the sense in which we say there's no evidence of satiation. There's no evidence of it running out at income level whatsoever."

(Wolfers' analysis spans multiple studies, but he says one of the recent Gallup polls he analyzed listed ">$500,000" as the highest income category.)

The upshot is that hedge fund honcho David Tepper would, in theory, need to earn an extra $400 million to see a 10 percent increase happiness. You, Bay Area median income earner, just need to find $5,000 more per year to make the same jump in your sense of well-being.

Tuesday

Flexible Lives, Flexible Rules

Contributing to a 401(k), getting two weeks of vacation or creating a health savings account are standard practice for many working adults. But standard doesn't work for Anand Gan and Landon Westbrook.

The duo, married four years, have spent much of their lives working temp jobs as they tried to make it big in New York City -- Mr. Gan as a drummer, bassist and guitarist, Ms. Westbrook in musical theater. While Ms. Westbrook has held down a few staff positions over the years, Mr. Gan says he's had only one "real" job.

Mr. Gan, 37, splits his time between his communications consulting firm, DT Media New York, and a music production company, Flytrap Music Production, which he co-owns. Ms. Westbrook, 38, works full-time for DT Media, which Mr. Gan founded nearly five years ago.

Because they rely on unpredictable project assignments, Mr. Gan and Ms. Westbrook must set aside a part of each check for taxes and business expenses before paying themselves. What they do get, they save. "It's always in the back of my mind, 'What if I never work again?' I have to have the money there," says Ms. Westbrook.

Mr. Gan and Ms. Westbrook live a relatively modest life, sharing a rent-stabilized ($1,350 a month) three-bedroom apartment with their 22-month-old son, Harrison. Flexible work schedules allow them to keep child-care costs low. The couple's biggest indulgence, they say, is fine food.

Mr. Gan and Ms. Westbrook each have traditional IRAs, worth a combined total of about $39,000. While they try to contribute the annual maximum allowance, they admit it doesn't always happen. "For us, these things are a priority, but sometimes other things get in the way," says Ms. Westbrook. Harrison's birth and some health issues forced them to forgo some IRA contributions.

Because of their need for fast funds in case work dries up, Mr. Gan and Ms. Westbrook keep the vast majority of their money in cash. They have $160,000 in the bank, though they are looking at putting some of that money into retirement accounts.

In addition to a few individual stocks and a small 401(k) from an old job, Ms. Westbrook also owns a cheap fixer-upper in Savannah, Ga., where she's originally from. She used proceeds from the sale of her old New York apartment to buy the house. A renter had been covering most of the costs, but that lease is ending and the house may sit empty for a few months before a replacement moves in. Ms. Westbrook and Mr. Gan talk of using the property as a second home in the future.

With all the cash and investments added up, says Ms. Westbrook, "It doesn't seem like a bad chunk of change. But we also couldn't quit working on that kind of money. It's better than nothing, I guess."

The couple says their plans grew more focused once Harrison was born, as they bought life insurance and started contributing to a 529 college savings plan. But they recognize it will be easier for him to find loans for school than it will be for them to do the same during retirement, so they haven't put much into the account.

ADVICE FROM THE PRO: Annette Clearwaters , a fee-only certified financial planner and president of New York-based Clarity Investments + Planning LLC, is impressed with how the couple holds the line on expenses. "It seems like they're self-disciplined in the spending area," she says.

To avoid situations when life events "get in the way" of contributing to retirement accounts, Ms. Clearwaters recommends setting up automatic deposits. She says Mr. Gan and Ms. Westbrook could take a certain percentage of each check and put it into their IRAs, just as they do for business expenses and taxes. Any consistent schedule is better than a lump sum, Ms. Clearwaters says. "If you wait till the end of the year, I don't think you'll ever be as successful in putting money aside," she warns.

She also recommends the couple look into opening a SEP IRA because of the higher contribution limits and tax benefits.

Ms. Clearwaters commends the couple for having saved so much and keeping it liquid, explaining that they should have up to 12 months of expenses set aside because they're both self-employed. She says they could invest in index funds, spreading contributions throughout the year. Ms. Clearwaters recommends a conservative allocation of 60% stocks and 40% bonds, since this is where they would turn if their cash runs low and business dries up.

Ms. Clearwaters says Mr. Gan and Ms. Westbrook could afford to put some more money into the college fund because they're sitting on so much cash, even if it's "some nominal amount" like $50 a month.

Article by Finance Yahoo

The duo, married four years, have spent much of their lives working temp jobs as they tried to make it big in New York City -- Mr. Gan as a drummer, bassist and guitarist, Ms. Westbrook in musical theater. While Ms. Westbrook has held down a few staff positions over the years, Mr. Gan says he's had only one "real" job.

Mr. Gan, 37, splits his time between his communications consulting firm, DT Media New York, and a music production company, Flytrap Music Production, which he co-owns. Ms. Westbrook, 38, works full-time for DT Media, which Mr. Gan founded nearly five years ago.

Because they rely on unpredictable project assignments, Mr. Gan and Ms. Westbrook must set aside a part of each check for taxes and business expenses before paying themselves. What they do get, they save. "It's always in the back of my mind, 'What if I never work again?' I have to have the money there," says Ms. Westbrook.

Mr. Gan and Ms. Westbrook live a relatively modest life, sharing a rent-stabilized ($1,350 a month) three-bedroom apartment with their 22-month-old son, Harrison. Flexible work schedules allow them to keep child-care costs low. The couple's biggest indulgence, they say, is fine food.

Mr. Gan and Ms. Westbrook each have traditional IRAs, worth a combined total of about $39,000. While they try to contribute the annual maximum allowance, they admit it doesn't always happen. "For us, these things are a priority, but sometimes other things get in the way," says Ms. Westbrook. Harrison's birth and some health issues forced them to forgo some IRA contributions.

Because of their need for fast funds in case work dries up, Mr. Gan and Ms. Westbrook keep the vast majority of their money in cash. They have $160,000 in the bank, though they are looking at putting some of that money into retirement accounts.

In addition to a few individual stocks and a small 401(k) from an old job, Ms. Westbrook also owns a cheap fixer-upper in Savannah, Ga., where she's originally from. She used proceeds from the sale of her old New York apartment to buy the house. A renter had been covering most of the costs, but that lease is ending and the house may sit empty for a few months before a replacement moves in. Ms. Westbrook and Mr. Gan talk of using the property as a second home in the future.

With all the cash and investments added up, says Ms. Westbrook, "It doesn't seem like a bad chunk of change. But we also couldn't quit working on that kind of money. It's better than nothing, I guess."

The couple says their plans grew more focused once Harrison was born, as they bought life insurance and started contributing to a 529 college savings plan. But they recognize it will be easier for him to find loans for school than it will be for them to do the same during retirement, so they haven't put much into the account.

ADVICE FROM THE PRO: Annette Clearwaters , a fee-only certified financial planner and president of New York-based Clarity Investments + Planning LLC, is impressed with how the couple holds the line on expenses. "It seems like they're self-disciplined in the spending area," she says.

To avoid situations when life events "get in the way" of contributing to retirement accounts, Ms. Clearwaters recommends setting up automatic deposits. She says Mr. Gan and Ms. Westbrook could take a certain percentage of each check and put it into their IRAs, just as they do for business expenses and taxes. Any consistent schedule is better than a lump sum, Ms. Clearwaters says. "If you wait till the end of the year, I don't think you'll ever be as successful in putting money aside," she warns.

She also recommends the couple look into opening a SEP IRA because of the higher contribution limits and tax benefits.

Ms. Clearwaters commends the couple for having saved so much and keeping it liquid, explaining that they should have up to 12 months of expenses set aside because they're both self-employed. She says they could invest in index funds, spreading contributions throughout the year. Ms. Clearwaters recommends a conservative allocation of 60% stocks and 40% bonds, since this is where they would turn if their cash runs low and business dries up.

Ms. Clearwaters says Mr. Gan and Ms. Westbrook could afford to put some more money into the college fund because they're sitting on so much cash, even if it's "some nominal amount" like $50 a month.

Article by Finance Yahoo

Wednesday

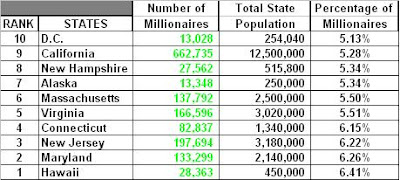

State with the most Millionaires

Happy St. Patrick's Day! I hope everyone has a bit of green on. If not, here's a little cyber pinch sent your way. I of course put on a cute green shirt along with some greenish eyeshadow.

Since it's St. Paddy's Day and the mood is green, let's talk about MONEY-honey-MONEY. A survey came out and reported a significant decline to the number of millionaires in America. Specifically from 5,607,989 in 2008 to 5,139,385 in 2009. But if you're one of them rich folks that's able to hold onto your ranking, kudos to you! Why? Because you're in the top 4.46%!

Keep in mind this excludes real estates. So that's very impressive!

As you know, I'm HOUSE rich but CASH poor. So I'm definitely not even close to being a millionaire. Surprisingly California is not #1 on the list but #9. It said that CA has the most millionaires but because our state has so many households, this dragged down our ranking. Can you guess which state is #1?

For more fun reading click here: The Richest States in America.

Since it's St. Paddy's Day and the mood is green, let's talk about MONEY-honey-MONEY. A survey came out and reported a significant decline to the number of millionaires in America. Specifically from 5,607,989 in 2008 to 5,139,385 in 2009. But if you're one of them rich folks that's able to hold onto your ranking, kudos to you! Why? Because you're in the top 4.46%!

Keep in mind this excludes real estates. So that's very impressive!

As you know, I'm HOUSE rich but CASH poor. So I'm definitely not even close to being a millionaire. Surprisingly California is not #1 on the list but #9. It said that CA has the most millionaires but because our state has so many households, this dragged down our ranking. Can you guess which state is #1?

For more fun reading click here: The Richest States in America.

Monday

Warren Buffett

Talk about living below one's mean.

The "Oracle of Omaha" Mr. Warren Buffet has been doing that for 52 years. That's almost half a century despite the fact that he's a billionaire, with 9 zeros.

Warren Buffett epitomizes living modestly in today's tough economic climate. Despite a $47 billion fortune, the legendary investor and the world's 3rd richest man lives in the same five-bedroom, gray stucco house he bought in Omaha, Nebraska's Happy Hollow suburb in 1958 for $31,500.

This folksiness is in line with his famous investing philosophy. "If you don't feel comfortable owning something for 10 years," he once told a reporter, "then don't own it for 10 minutes."

Few billionaires are as frugal. Even in these tough times, modesty is a relative term among the super rich.

Friday

paying down credit cards and not the Mortgage

Here's an interesting article detailing the fact that many U.S. consumers are skipping payments to their mortgage just to use the funds available to pay off their credit card.

U.S. consumers are starting to look like a frugal, debt-fearing lot as they pay down billions of dollars in credit-card obligations. But an alarming trend is emerging: A small but growing number of people are skipping mortgage payments in favor of paying their credit-card bills.

In an unprecedented shift, for some consumers having a credit card in good standing appears to have taken priority over having a roof over one's head, experts said.

While overall consumer debt rose unexpectedly in January, consumers continued to pay off their credit cards that month -- a record 16th straight month of lower credit-card debt -- with such debt dropping about $1.7 billion to $864.4 billion, according to the Federal Reserve on Friday. For further reading, click here.

U.S. consumers are starting to look like a frugal, debt-fearing lot as they pay down billions of dollars in credit-card obligations. But an alarming trend is emerging: A small but growing number of people are skipping mortgage payments in favor of paying their credit-card bills.

In an unprecedented shift, for some consumers having a credit card in good standing appears to have taken priority over having a roof over one's head, experts said.

While overall consumer debt rose unexpectedly in January, consumers continued to pay off their credit cards that month -- a record 16th straight month of lower credit-card debt -- with such debt dropping about $1.7 billion to $864.4 billion, according to the Federal Reserve on Friday. For further reading, click here.

Tuesday

Prize: a $2,000,000 house

Hello everyone, sorry that I've been MIA. Work has kept me busy. Usually around this time, I have to prepare financial statements to be sent out to all our clients. Before the release, all financial data has to be checked for accuracy. This is a long and tedious process so it's kept me from blogging.

I came across this article in our local news about a raffle winning of this $2 million home a few miles away from San Francisco. It is actually located across from the famous Golden Gate Bridge in a very expensive upper middle class community. The person who won this is only 26 years old. I heard from a friend who knows of this winner that he only purchased 2 raffle tickets for a total of $300. Can you imagine the luck he had a few hundred dollars into a couple million dollars? I knew about this raffle from advertisements and commercials, but never did I imagine that this was a legitimate contest.

He has the choice to either move into this $2 million house which would require him to pay $22,000 in property tax a year. Which is not bad if you think about it as being $1,833/mo which is far less than a monthly mortgage on a single family home. His other choice is to redeem the cash prize of $1,600,000.

If you were him, which choice would you make?

I would highly consider the sweeping view of the SF Bay in this nice and secluded neighborhood. Moreover, the monthly payment is less than 1/2 of my $3500/mo mortgage which is a plus. However, it would cost me $6 every time I cross the Golden Gate Bridge back into the city. Alright, Mrs. Bee can dream!

Click here for more reading: $2million Larkspur Home

Thursday

Stay the course with your 401K

I learned a huge lesson since the start of the recession in early 2009. No matter what happens to the financial markets, don’t stop contributing to your 401K. In fact, during a downturn and when everyone panics, we should be doing the opposite. Stay calm and invest like there's no tommorrow. The real winners are the ones that goes against the crowd; the non-herd followers. I know many coworkers, friends, and family panicked when the financial market was spiraling out of control. For example, my mother did not feel safe during that time with her investment choices. She invested in mid caps, large caps, and foreign funds. With her balance decreasing daily, she panicked and moved all her money out of these funds and into more stable ones. By her action, I felt she had declared defeat by realizing a loss. Had she left her investments alone until today, she would have been able to recoup most of the negative return during that time.

What have I learned from this? I learn that the following three formulas matter in order to stay the course to a healthy retirement: Savings, Employer contributions, and Prudent investing.

Savings. Continue to invest in your retirement account and ignore the performance of the current market. Don’t stop saving. In fact, save at least 10% if you can or better up to the maximum allowed.

Employer contributions. Take advantage of free money your company has to offer you. If your employer matches 6% to the dollar, try to contribute up to this 6% in order to get the match.

Prudent investing. Keep stashing away cash from each of your paychecks. Stay the course and don't get distracted from all the negative news around you. Retirement money is here to stay and for the long run. 1 to 2 years of bad returns should not have an impact to your retirement approach. Most importantly, remember to diversify and not put all your eggs in one basket. And above all, be patient and give it time so your money can grow.

Loyal financial bee followers, what is your approach to your 401K?

Friday

Valentine's Day can complicate finances

Love is in the air! It's almost Valentine's Day. Everyone is giddy and in a romantic mood. But for some, this may spell doom especially for the couples that are never on the same financial page.

I'm glad DH and I are pretty much on the same page with our perspective towards money and the way we handle our finances. But I do admit turbulent times during our dating years and early marriage life. We'll be celebrating our 3rd Anniversary in October.

We recently refinanced our house so I was able to get a report on my credit score. Mine is 805 and DH's is 780. I believe the reason for my high score is due to a luxury vehicle I had financed 6 years ago. It was later paid in full shortly after. This may have contributed to a bump in credit score and also by paying off my credit card in full every single month.

Looking back, we did not enter into a marital agreement until we both made decent money. Our income has doubled in this 3 year span. Not just that, we did not commit into buying a house together until we both had stability in our jobs, comfortable incomes, and a decent down payment.

We fight about money from time to time. DH feels I spend money frivolously. He was raised with a conscience to spend money wisely and carefully. He does have his occasional splurge here and there but not as often as I. Although he makes around 60%of the income, I admire him with his money principles because he can easily afford to spend recklessly, but he doesn't. Therefore, we make a great team together. I remind him to spend sometimes while he motivates me to save a bit.

Wednesday

$900,000 of fraud money

Okay, I know $70 is not alot of money since that is the amount siphoned from my credit card by an unknown intruder. It is a pea-sized concern compared to Dave's massive fraud amount in this featured story. But a theft is a theft no matter what the amount is. It is the intention that has me worried. So here lies another interesting article related to ID fraud. This horrible event is so prevalent that it is happening every minute of the day to someone.

IDENTITY THEFT AND FRAUD HAVE RUNIED DAVE CROUSE'S LIFE

In fewer than six months, some $900,000 in merchandise, gambling and telephone-services charges were stolen out of his debit card. His attempts to salvage his finances have cost him nearly $100,000 and have bled dry his savings and retirement accounts. His credit score, once a strong 780, has been decimated. And his identity – SS#, address, phone numbers, even historical information - is still being used in attempts to open credit cards and bank accounts. The new credit card rules that go into effect on Feb. 26, 2010 are supposed to protect you, but will they?

"I have no identity," said Crouse, 56. "I have no legacy. My identity is public knowledge and even though it's ruined, they're still using it. "It really ruined me," he said. "It ruined me financially and emotionally."

Crouse is among the 11.1 million adults - one in every 20 U.S. adults - last year who have the dubious distinction of breaking the record of the number of identity-fraud victims in the U.S., according to a recent study. The cost to the victims: a collective $54 billion. The odds have never been higher for becoming a fraud victim. It's an easy crime to perpetrate, a crime that's almost impossible to catch when done in a sophisticated manner and a crime in which enforcement is very limited.

Endless paperwork

Crouse can attest to that. Once an avid fan of online shopping and banking, the Bowie, Md., resident would auction on eBay.com, download songs from iMesh.com and use his ATM card like a credit card. He first noticed suspicious activity in his account in February of 2009 for small charges of $37 or $17.98. He had a full-time job then and was spending out of an account that generally held $30,000. "All of a sudden it really got bad," he said. "In August the charges hit big time -- $600, $500, $100, $200 - all adding up from $2,800 to $3,200 in one day."

He called his bank immediately and started what began a tiresome process of filling out what he said finally amounted to about 20 affidavits swearing that he was not responsible for the charges. He said one day he filled out an affidavit about a charge and the next day the bank had accepted similar charges approaching $4,000.

Now he is in double jeapordy after being unemployed: His $2,300 a week net income had dwindled to $780 in unemployment checks every two weeks and his accounts were getting drained daily - even after he closed his debit account. He opened a new account at a new bank and the next day both accounts got hit with a $1,100 charge. The new bank told him it was keystroke malware that had likely done him in. Someone had hacked into one of the sites he visited regularly, his computer got infected and picked up all his personal information by tracking every key he struck.

While much of the fraud came from online purchases and at gambling sites, there were new accounts opened in different names but linked to his bank account. There was one purchase of a plasma TV from a Best Buy in Florida that was shipped to a New York address. In another case a woman in North Carolina was writing out checks tied to his account.

High-value targets

Identity thieves steal mostly through two means. They take an established address and phone number of an identity that "has some value," like a doctor or a lawyer. In many instances, they can go to the Internet and acquire the matching Social Security number for as little as $50. They then have enough information to get an address changed with your bank account or a credit card account. They apply for new accounts as you. Others take over existing accounts through keystroke malware that you - and probably hundreds or even thousands simultaneously - have picked up through the Internet. Listening software then sits on your computer, perking up when you go to a bank site. It copies all your key strokes -- your user name, password, challenge question, account numbers, everything.

IDENTITY THEFT AND FRAUD HAVE RUNIED DAVE CROUSE'S LIFE

In fewer than six months, some $900,000 in merchandise, gambling and telephone-services charges were stolen out of his debit card. His attempts to salvage his finances have cost him nearly $100,000 and have bled dry his savings and retirement accounts. His credit score, once a strong 780, has been decimated. And his identity – SS#, address, phone numbers, even historical information - is still being used in attempts to open credit cards and bank accounts. The new credit card rules that go into effect on Feb. 26, 2010 are supposed to protect you, but will they?

"I have no identity," said Crouse, 56. "I have no legacy. My identity is public knowledge and even though it's ruined, they're still using it. "It really ruined me," he said. "It ruined me financially and emotionally."

Crouse is among the 11.1 million adults - one in every 20 U.S. adults - last year who have the dubious distinction of breaking the record of the number of identity-fraud victims in the U.S., according to a recent study. The cost to the victims: a collective $54 billion. The odds have never been higher for becoming a fraud victim. It's an easy crime to perpetrate, a crime that's almost impossible to catch when done in a sophisticated manner and a crime in which enforcement is very limited.

Endless paperwork

Crouse can attest to that. Once an avid fan of online shopping and banking, the Bowie, Md., resident would auction on eBay.com, download songs from iMesh.com and use his ATM card like a credit card. He first noticed suspicious activity in his account in February of 2009 for small charges of $37 or $17.98. He had a full-time job then and was spending out of an account that generally held $30,000. "All of a sudden it really got bad," he said. "In August the charges hit big time -- $600, $500, $100, $200 - all adding up from $2,800 to $3,200 in one day."

He called his bank immediately and started what began a tiresome process of filling out what he said finally amounted to about 20 affidavits swearing that he was not responsible for the charges. He said one day he filled out an affidavit about a charge and the next day the bank had accepted similar charges approaching $4,000.

Now he is in double jeapordy after being unemployed: His $2,300 a week net income had dwindled to $780 in unemployment checks every two weeks and his accounts were getting drained daily - even after he closed his debit account. He opened a new account at a new bank and the next day both accounts got hit with a $1,100 charge. The new bank told him it was keystroke malware that had likely done him in. Someone had hacked into one of the sites he visited regularly, his computer got infected and picked up all his personal information by tracking every key he struck.

While much of the fraud came from online purchases and at gambling sites, there were new accounts opened in different names but linked to his bank account. There was one purchase of a plasma TV from a Best Buy in Florida that was shipped to a New York address. In another case a woman in North Carolina was writing out checks tied to his account.

High-value targets

Identity thieves steal mostly through two means. They take an established address and phone number of an identity that "has some value," like a doctor or a lawyer. In many instances, they can go to the Internet and acquire the matching Social Security number for as little as $50. They then have enough information to get an address changed with your bank account or a credit card account. They apply for new accounts as you. Others take over existing accounts through keystroke malware that you - and probably hundreds or even thousands simultaneously - have picked up through the Internet. Listening software then sits on your computer, perking up when you go to a bank site. It copies all your key strokes -- your user name, password, challenge question, account numbers, everything.

Identity fraud on the rise - up 12% to 11.1 million adults affected in 2009

There was an article that came out today pointing out the severity of identity theft. As you all know, I fell victim to this sort of fraud a few days ago. It amazes me that up to 11.1 million people are affected by this silent and invisible crime. But it comes at no surprise since society nowadays rely so heavily on credit cards and other form of identifications for transactional purposes.

So please remember to reconcile your financial statements on a monthly basis to make sure all transaction are accounted for. You should also request from the credit bureaus to send a report showing the number of credit cards open under your name. And when making purchases on the internet, be sure to check if the site is secured. Lastly, I know how we all hate getting spam/junk letter mails soliciting us to apply for credit cards. Before throwing them in the recycle bin, shred them in a paper shredder first.

Be Safe and Happy Spending!

To become rich, stop acting like it

We all fall victim from time to time with the "Keeping up with the Joneses" effect. I admit, quite often than not, to having a hard time differentiating between my NEEDs versus my WANTs. Thus, by the hopes of me blogging and bringing awareness of my spending to light, I hope to dampen this urge. I remind myself that delayed satisfaction is the key to becoming rich in the long run.

I'm currently reading this book called "Stop Acting Rich . . . and Start Living Like a Real Millionaire" and would like to share a few interesting facts.

Fact #1: 86% of all luxury vehicles are driven by people who are not millionaires.

Mrs. Bee response: True! I drive an old luxury vehicle and I am no where near miilionaire status (YET). But I hope to be one day in hopes to become that 14% that is a millionaire who continues to drive a luxmobile.

Fact #2: $16 is what most millionaires pay for a haircut

Mrs. Bee response: False! I'm so guilty of paying around $55 for a nice haircut every 6 months. Again, it goes to show I am not a millionaire (YET). However, this excerpt is misleading because some places around town charges less than $16 (tips included) for haircuts. And those people sure don't look like millionaires or are they!

Fact #3: The #1 shoe brand worn by millionaire women is Nine West. Their favorite clothing store is Ann Taylor.

Mrs. Bee response: This again I feel is misleading. Nine West shoes are not cheap nor are Ann Taylor clothing. I don't own either brands so again this proves that I not a millionaire but my shoes are compareable to their prices.

The author points out that many people end up in financial trouble because they PRETEND to be rich. He believes there is a cure to this pretentious disease and quotes "But for the treatment to work, you must take a cold hard look at your balance sheet and at your life, and determine if you would be wealthier if you would stop acting rich."

Do you agree that there are way too many people in this soceity that act and pretend to be rich? Will the recession motivate pretenders to hit the reset button and not just act rich but live modestly like many real millionaires?

Please share your thoughts.

Tuesday

Where Are the Women on Wall Street?

Scroll down below to read the article. In the meantime, here's my reaction:

Mrs. Bee's reaction: This featured article has some substance to the truth. A few year's back before this current job of mine, I landed a FT position with this hedge fund company. To my surprise, it was a small size firm with less than 30 employees. All of them were men except for myself, my manager, and the receptionist being the only women. (Can we say too much testosterone and not enough estrogen?) However, I did find another FT job shortly after working at my current job. That job just didn't work out the way I had hope mainly due to the long distance commute. But I was surprised by the ratio of the gender inequality.

You will also notice if you tune into MSNBC in the morning where they show the trading floor of the NYSE, not only is the floor littered with paper, but also MEN. There is hardly a women in sight except perhaps for a reporter on site. My DH works on the trading floor and he admits that his coworkers consist of all male. Do you see this kind of disparity in your workplace or anywhere else?

Here's the article:

When Sallie Krawcheck was hired six months ago as president of global wealth and investment management at Bank of America, she was besieged with e-mail messages from current and former Wall Street women celebrating her return to the fray.

The outpouring over Ms. Krawcheck’s return reflects deep anxiety among women in the financial industry that their career paths are narrowing even as business picks up again. Women have always been drawn to finance in smaller numbers than men. But after nearly two decades of increased hiring and promotion of women on Wall Street, their ranks appear to be shrinking again.

Even though women are gaining ground on men enrolled in business school — they constituted 39.3 percent of full-time students in American business schools in 2009, compared with 34.1 percent five years earlier, according to the Association to Advance Collegiate Schools — the percentage of those women headed for finance or accounting jobs is dropping.

Of those female graduates, 21.1 percent were pursuing finance or accounting in 2009, down 6.6 percentage points from 2005, according to the Graduate Management Admission Council, a nonprofit group of business schools. The rate also dropped for men, but less drastically — falling 4.7 percentage points this year to 25.4 percent.

But in the heart of Wall Street, the aggressive environment on the trading floor is often cited as a reason that women are rare at the top. Others cite the dearth of women to aid in career networking. Whatever the reason, ascending the ladder is much harder for women, said Bruce C. Greenwald, a professor of finance and strategy at Columbia University Business School.

“It is more difficult for women to come back because the environment in financial institutions is generally more hostile to women,” he said. “This culture has developed over a very long period of time, and it has been exacerbated as the firms’ emphasis has shifted from traditional investment banking to sales and trading, which is an even more macho culture.”

Sunday

til DEBT do us part

I have no kids so spending is just between DH and I. However, we tuned into an episode of MSNBC called "Til Debt do us part" where a financial wizard name Gail helps families get out of debt by altering their destructive spending habits.

On this episode, she follows a couple with $25K worth of credit card debt. The wife is a SAHM with 2 young kids and a baby on the way. Her husband is the sole provider of the family earning $80K annually. So this is a family of 4 soon to be 5 living on merely $80,000 per year. What bothered me was that they seem oblivious to their current financial crisis. They continued to live a care free high consumption lifestyle. They spend on average $900/mo on organic food. The wife does not drive so she pays an additonal $120/mo to have food delivered to their house. Add in the mortgage, entertainment, utility/gas, and other kid expenses, we can all see why this couple was bleeding red. When confronted by Gail with a money makeover, they felt nothing was wrong because they were able to keep up with the credit card payment. But we soon discover that their payment was only on the interest portion.

This family was clearly out of control and not in touch with planning and budgeting. Spending $900/mo on organic food was mind blowing. On top of that, another $120 for delivery services. Just this $1,020 in expense already equates to my monthly spending in food/entertainment/utility/etc. We make 1.5 times more than this family but spend much much less. It goes to show that there are many couples out there either in denial or blindsided by their financial reality. This show serves as a great purpose to motivate families to get out of debt. Planning and saving for a secure future is more important than high consumption. Especially if there are children involved.

On this episode, she follows a couple with $25K worth of credit card debt. The wife is a SAHM with 2 young kids and a baby on the way. Her husband is the sole provider of the family earning $80K annually. So this is a family of 4 soon to be 5 living on merely $80,000 per year. What bothered me was that they seem oblivious to their current financial crisis. They continued to live a care free high consumption lifestyle. They spend on average $900/mo on organic food. The wife does not drive so she pays an additonal $120/mo to have food delivered to their house. Add in the mortgage, entertainment, utility/gas, and other kid expenses, we can all see why this couple was bleeding red. When confronted by Gail with a money makeover, they felt nothing was wrong because they were able to keep up with the credit card payment. But we soon discover that their payment was only on the interest portion.

This family was clearly out of control and not in touch with planning and budgeting. Spending $900/mo on organic food was mind blowing. On top of that, another $120 for delivery services. Just this $1,020 in expense already equates to my monthly spending in food/entertainment/utility/etc. We make 1.5 times more than this family but spend much much less. It goes to show that there are many couples out there either in denial or blindsided by their financial reality. This show serves as a great purpose to motivate families to get out of debt. Planning and saving for a secure future is more important than high consumption. Especially if there are children involved.

Subscribe to:

Posts (Atom)